Home, Auto & Life coverage for Wichita, Kansas City, Topeka, Overland Park

Kansas personal insurance provides essential protection across the Sunflower State. From the I-35 corridor through Kansas City to the agricultural plains surrounding Wichita and the state capital in Topeka, Dream Assurance Group helps Kansas residents navigate the unique challenges of convective storm season (April-September) with tornado, wind, and hail exposures. Compliance with Kansas Statute 40-3107 is mandatory for all drivers. We provide comprehensive coverage tailored to Kansas regulations and lifestyle needs.

Comply with Kansas Statute 40-3107 no-fault PIP mandates (25/50/25 liability + $4,500 Medical PIP). We ensure your policy meets Kansas requirements while offering competitive rates from Kansas-approved carriers.

View Auto Coverage

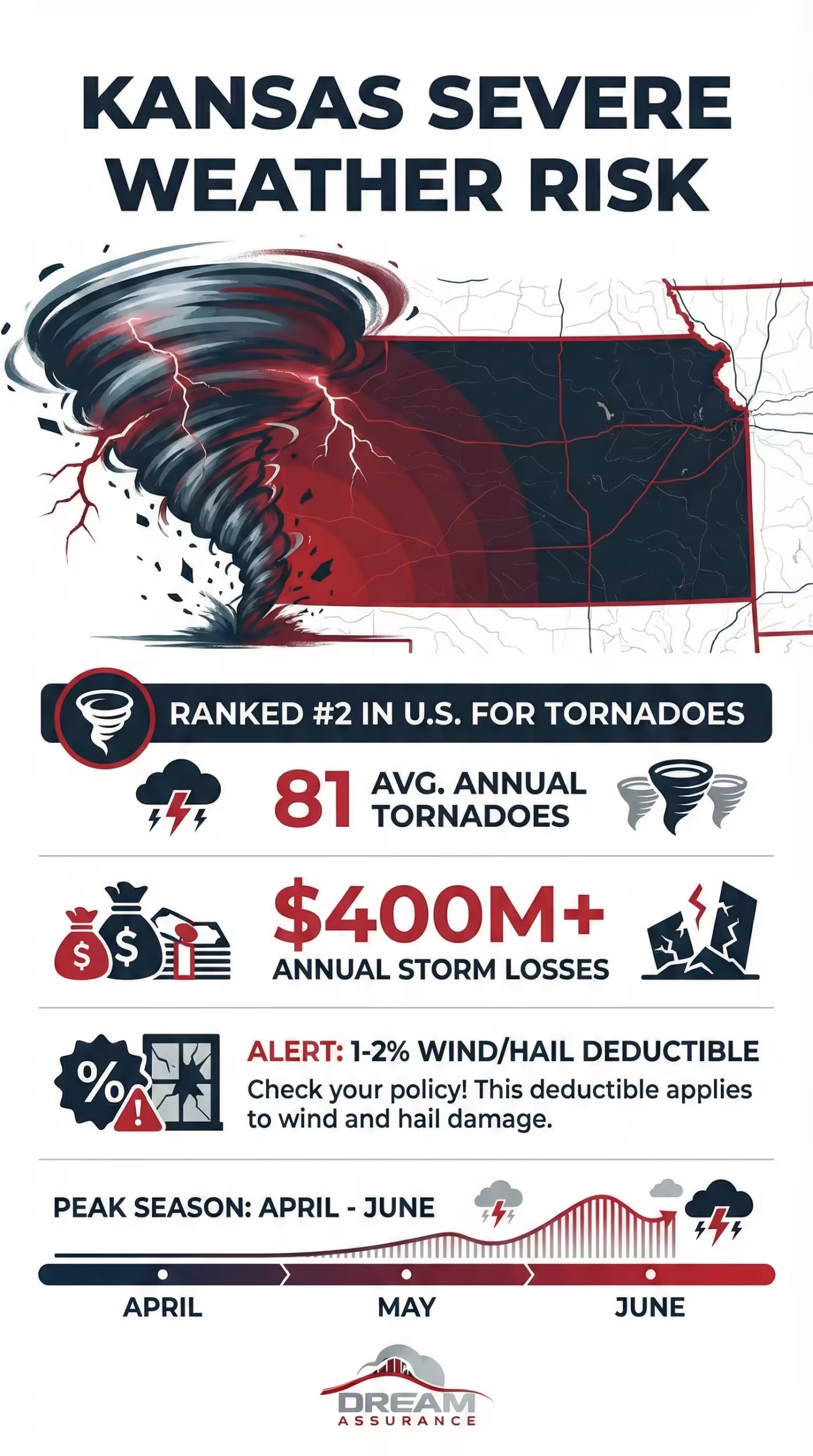

Guaranteed Replacement Cost (RCV) coverage for Kansas homes exposed to convective storm risks including tornadoes, severe hail, and wind events. Kansas averages 81 tornadoes annually (based on average annual number of tornadoes per state data between 1994 and 2023) —protect your investment with full reconstruction coverage.

View Home Coverage

HO-6 coverage for unit owners. Protects interior and personal property.

View Condo Coverage

Protect your personal property from theft, fire, or storm damage in your rented apartment or home. Essential coverage for Kansas college towns like Lawrence and Manhattan where renters face similar convective weather risks as homeowners.

View Renters Coverage

Term or Permanent Life insurance options to protect your family's future.

View Life Coverage

Additional liability protection of $1M+ to safeguard your assets.

View Umbrella Coverage

Save up to 25% when you bundle your home and auto policies together.

View Bundle Savings

Coverage for veterinary bills to keep your furry family members healthy.

View Pet CoverageKansas is a "no-fault" state for injuries. Drivers must maintain the following liability coverage, known as "25/50/25":

Per Kansas Statute 40-3107, the state requires the following:

PIP: $4,500 Medical PIP required.

No-Fault: PIP covers medical expenses, lost wages, and essential services regardless of fault, reducing litigation and speeding claims resolution.

Uninsured Motorist: Recommended—according to Insurance Information Institute, Kansas has a 12.0% (in 2023) uninsured driver rate.

Unlike auto insurance, the State of Kansas does not legally mandate homeowners insurance. However, if you have a mortgage, your lender will require proof of insurance.

Coverage Recommendation: In Kansas' volatile climate, Guaranteed Replacement Cost (RCV) ensures full reconstruction cost without depreciation, unlike Actual Cash Value (ACV) which deducts wear and tear.

Identify Kansas-specific exposures: tornado alley location, flood zone status, convective storm frequency, and asset protection levels.

We compare Kansas-specific rates from carriers familiar with local risk profiles including Travelers, Nationwide, and other A-rated insurers.

Evaluate Kansas compliance: PIP limits ($4,500 Medical), 25/50/25 liability, wind/hail deductibles, replacement cost vs. ACV, and carrier financial strength.

Same-day policy issuance with immediate proof of insurance for lender or DMV requirements. Kansas Statute 40-3107 compliance verified.

Get Sunflower State coverage from a local agent.